Game Change: Infrastructure Growth Accelerating with AI

Game Change: Infrastructure Growth Accelerating with AI

The growth outlook for listed infrastructure continues to improve in 2024. Companies have been key beneficiaries of a virtuous cycle of generative AI development. We have seen increased profitability for datacenters themselves, rising estimates of future capacity installations, and surging forecasts for power demand and the utility investment needed for service. With this update, we review:

1. The extraordinary rise in utility earnings expectations following increased investment demand.

2. The need for infrastructure as an “all of the above” solution to service generative AI.

3. The discounted valuations for listed infrastructure and the prospects for total return.

Accelerating Utility Earnings Expectations

Current regulated utility earnings growth estimates are without precedent. Historically, regulated utilities in the U.S. were moderate growers. With the retirement of coal plants, the replacement with natural gas, and the penetration of renewables, investment levels increased and growth improved.

Today’s generative AI needs represent a “game change” for the utility sector. As of September 2024, estimates for datacenter power demand call for a quadrupling of 2023 levels by 2030, representing over 600 terrawatt hours and 11-12% of total U.S. power demand.

With associated levels for utility power demand growth rising, we expect a doubling in U.S. utility investment by 2026 compared to 2015 levels. With higher investment, we expect utility earnings to accelerate. Notably, our forecasts do not consider a dramatic increase in the profitability or the “regulated returns” (based on costs of capital) allowed for utilities. These should have an additional upward bias in a future period where long-term interest rates average higher than in the previous decade; in 2024, we have already seen an upward bias for utility authorised ROEs compared to 2023 and 2022 levels.

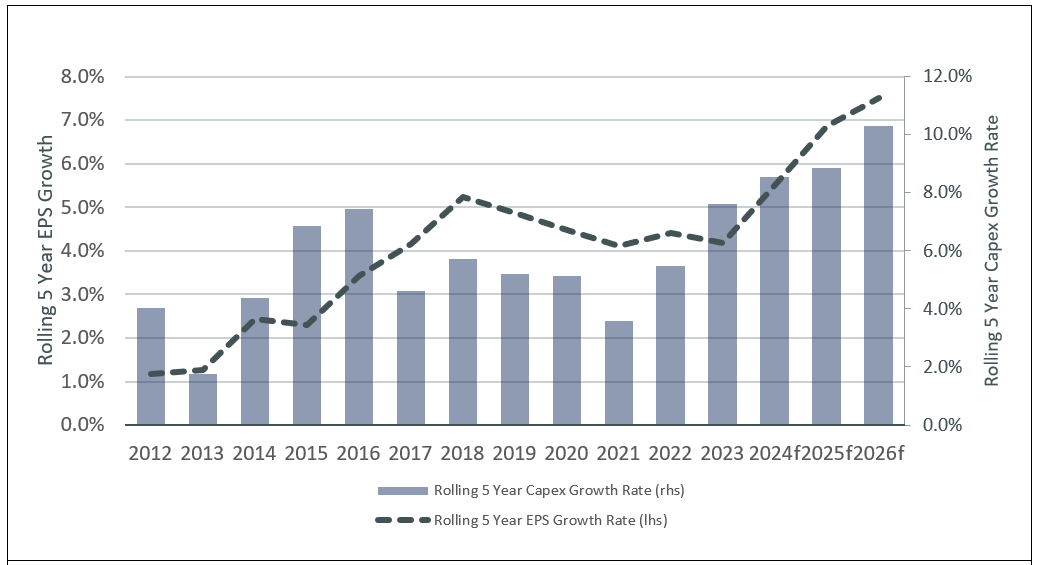

Rising Utility Growth: Earnings Follows Investment

Source: CBRE Investment Management. Capex forecasts per Edison Electric Institute and CBRE Investment Management forecasts, informed by aggregate rate base growth expectations. Earnings forecasts per CBRE Investment Management as of September 2024.

We see average long-term utility growth estimates as having the potential to reach a high single digit rate in the next two years. This is a dramatic change from a decade ago. On top of this potential, we see the possibility for both upward revisions and an increased duration to these growth expectations. At the utility level, planning for datacenter power capacity is extending into the latter half of this decade and beyond. We see increasing evidence of utilities rationing current power distribution to datacenters pending the start-up of new transmission; others have noted reduced transmission capacity through 2030; others see flagship assets as constrained by 2028 and are seeking “take-or-pay” contracts to support new transmission infrastructure. In the current environment, we clearly see a likelihood for enhanced utility investment over an extended period.

Infrastructure as an "All of the Above" Solution

We see diverse forms of energy, and diverse sectors across infrastructure as needed to service generative AI. In the last several months, we’ve seen announcements for the restart of nuclear generation for the first time in U.S. history, with some announcements linked to long-term power purchase agreements from large technology companies. Even before the rise of generative AI, we expected the contributions of nuclear energy, renewable generation, and traditional hydrocarbons capacity as needed to meet future global demands. The need for comprehensive energy supply is only enhanced in a post AI world.

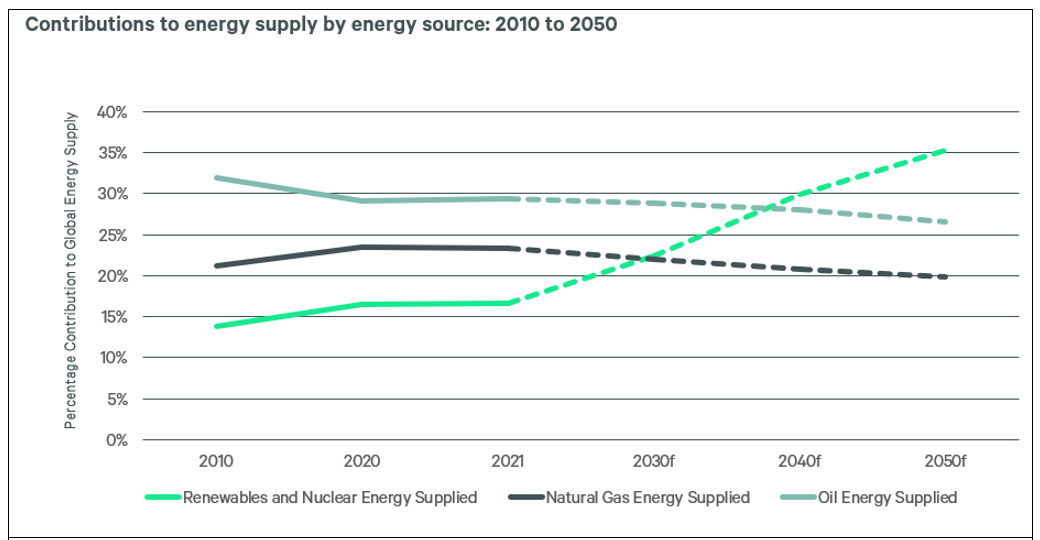

Renewables, Nuclear, and Traditional Hydrocarbons All Needed to Meet Future Energy Supply Needs

Source: CBRE Investment Management IEA (2022), World Energy Outlook 2022, IEA, Paris. Information is the opinion of CBRE Investment Management, which is subject to change and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Forecasts and any factors discussed are not a guarantee of future results.

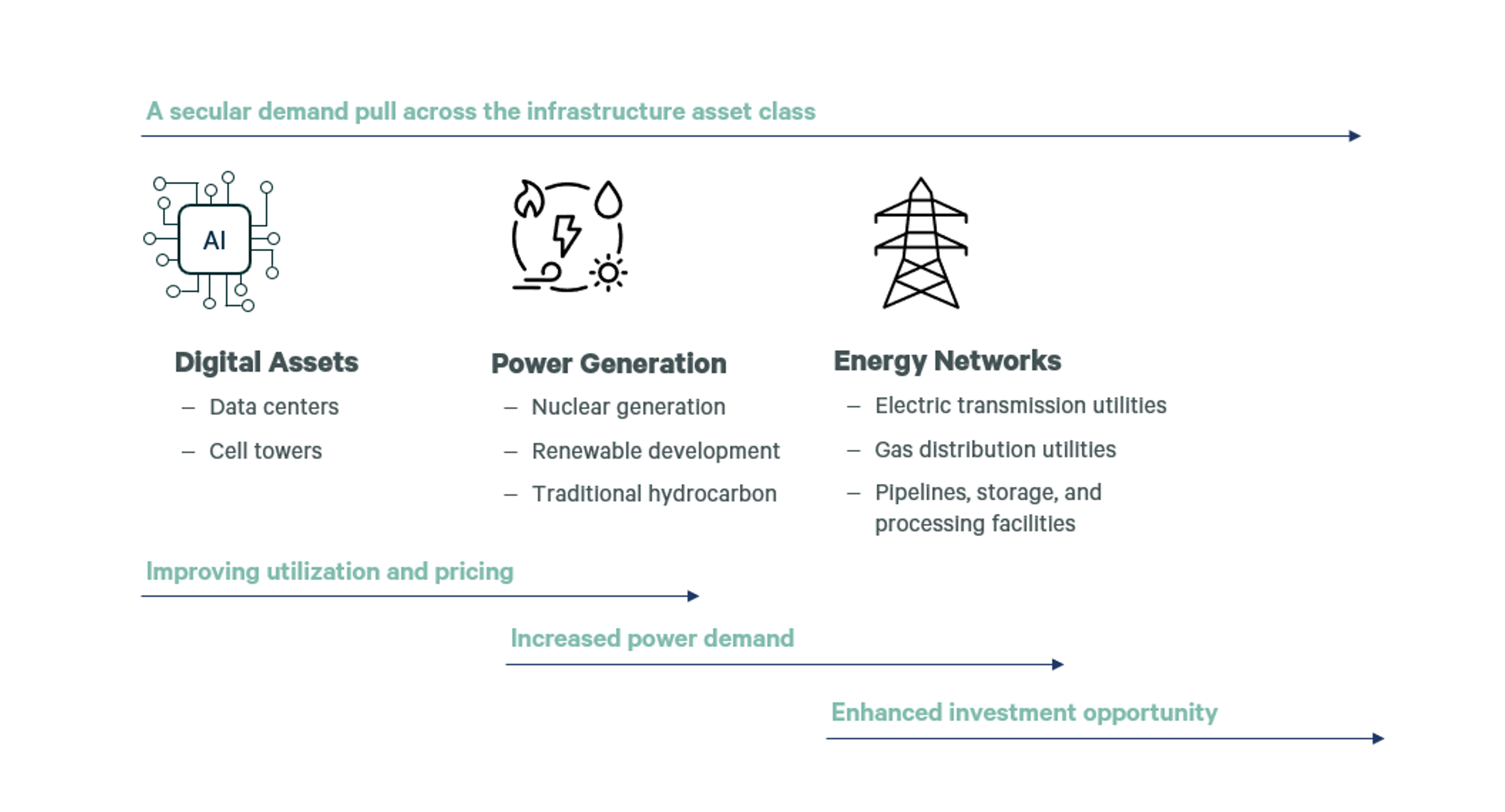

Across the infrastructure asset class, we believe the beneficiaries of generative AI are well placed. Communications infrastructure companies are seeing stronger growth, alongside the benefits of moderately lower borrowing rates. Contracted energy generation and renewable development are prospering in a new upcycle, while the need for energy transmission and transport remains strong.

When rolled up to the asset class level, we see infrastructure’s earnings are trending at approximately 300bps above their historic average, driven by infrastructure as an “all of the above” solution for generative AI.

Infrastructure as an “All of the Above” Solution for AI

Source: CBRE Investment Management. Information is the opinion of CBRE Investment Management, which is subject to change and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Forecasts and any factors discussed are not a guarantee of future results.

Compelling valuations and potential total returns

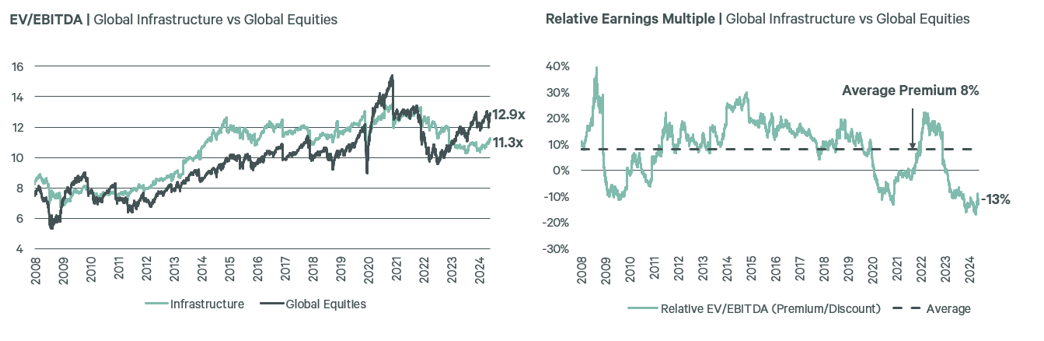

Listed infrastructure’s above average earnings growth is a key consideration in its ability to generate above average returns in the years ahead. The starting point for investors, that of current discounted valuations, is also key. As of Q3 2024, listed infrastructure’s earnings multiple, despite high single digit earnings growth, still trades at a large discount to broad equities. The asset class offers high income, discounted valuations to private markets, and is one of the larger historical beneficiaries of cuts in global central bank borrowing rates.

As we look ahead, we are optimistic for the asset class to eclipse the historical 8-10% total returns it has generated over the course of the last decade. We believe now is the perfect time to reassess portfolios and ensure that listed infrastructure is a strategic part of the investment mix. With its strong growth potential and compelling valuations, positioning listed infrastructure could be key to achieving strong returns in the years ahead.

Compelling valuations

Global Infrastructure trades at a discount rate to global equities

Source: CBRE Investment Management, iShares MSCI ACWI ETF, SDPR S&P Global Infrastructure ETF, proShares Dow Jones Brookfield Global Infrastructure ETF, of 08/31/2024. Information is the opinion of CBRE Investment Management, which is subject to change and is not intended to be a forecast of future events, a guarantee of future results, or investment advice. Forecasts and any factors discussed are not guarantee of future results.

Learn more about CBRE Investment Management

For more information on CBRE Investment Management and their funds and strategies visit their website.